PEARL PRL: Why Proof-of-Useful-Work Could Finally Matter

ANALYSIS | FIRST LOOK | June 2026 | crypto-lowcap.com

A first fundamental look at the project claiming to make GPU-based AI compute the new Bitcoin mining, and why the gap between thesis and on-chain reality is the only question that matters.

By Rowenta01 | crypto-lowcap.com | @CryptoRowenta01

#PoUW #MatMul #AICompute #PoW #ZKProofs #Lowcap #Bitcoin #GPU #PRL #PEARL

Before we start

This article does not constitute investment advice. These are purely personal observations from a fundamental analyst who has been covering the privacy and low-cap crypto space since 2016. Micro-cap and low-cap projects carry significant risk. The project described here is extremely young, unaudited, and carries a very high speculative risk profile. Do your own research.

The idea that stopped me

I have followed Proof-of-Work projects since 2016. I have seen hundreds of projects claim to make mining useful. Most of them failed. Primecoin searched for prime numbers. Curecoin folded proteins. None of them managed to create a durable economic loop between the ‘useful work’ and the blockchain’s security. That problem was considered essentially open.

Then, in April 2025, three researchers from the Hebrew University of Jerusalem and Princeton published a paper on IACR ePrint titled ‘Proofs of Useful Work from Arbitrary Matrix Multiplication’. A year later, one of the co-authors, Omri Weinstein, launched a mainnet. That project is PEARL.

The thesis is seductive in its simplicity: matrix multiplication, the central operation behind every large language model, every AI training run, every inference call, is already happening at massive scale across thousands of data centers. What if those GPU cycles could simultaneously secure a blockchain? What if each kilowatt-hour spent on AI inference could produce a native token as a byproduct, with no additional computational cost?

That is the 2-for-1 promise. And it is the kind of idea that deserves serious analysis, not hype.

My job here is to walk you through both possibilities, with cross-checked data and a clear verdict at the end. Because there is also a very serious counter-signal, a June 2026 empirical study that claims to have measured zero useful AI computation on the live network. And that is not a detail.

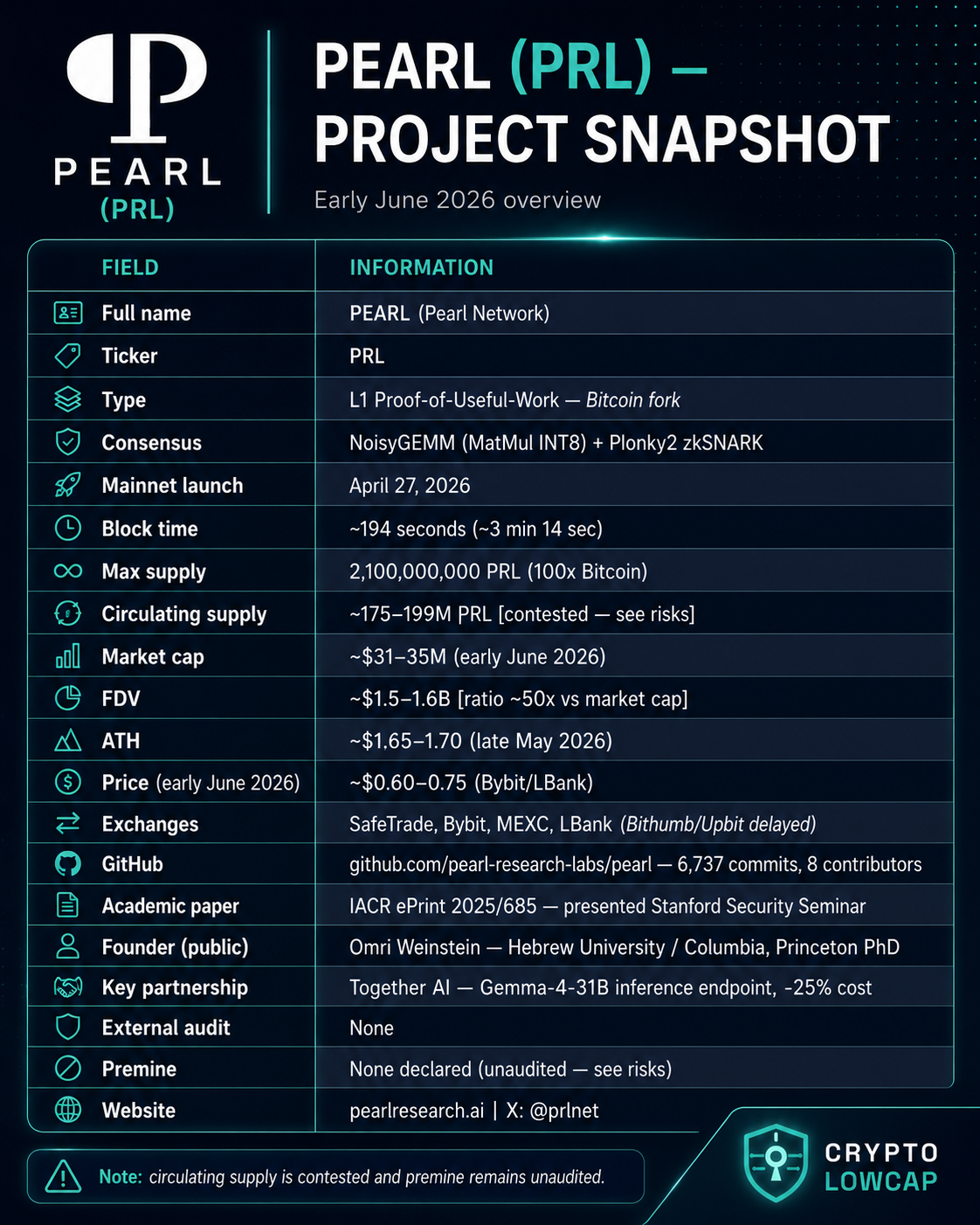

Project snapshot (data as of early June 2026)

1. The technology: what NoisyGEMM actually does

Let me be honest about something: the core mechanism of PEARL is technically non-trivial, and that is actually one of its genuine strengths. Most ‘AI + blockchain’ projects I have seen over the past three years are pure narratives, with no real cryptographic substance. PEARL is different, at least on the technical design paper.

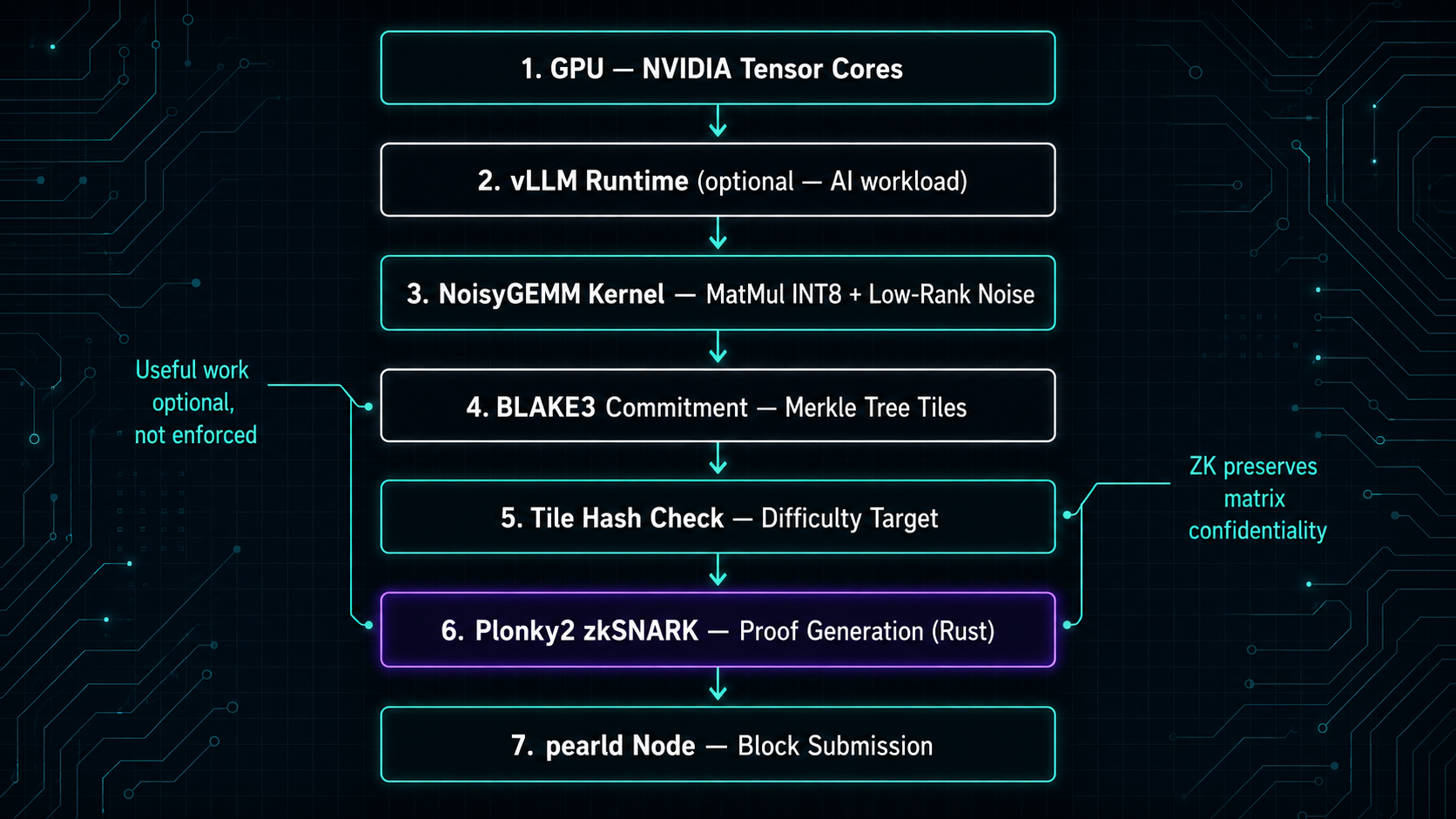

The protocol is built on a concept called NoisyGEMM, General Matrix Multiply with injected noise. Here is how it works at a functional level, stripped of the cryptographic formalism:

- The miner commits to two matrices A and B via BLAKE3 hash trees.

- Low-rank noise matrices E and F are deterministically generated from that commitment and the current chain state.

- The miner computes (A+E).(B+F), tile by tile, on GPU.

- Each tile produces an intermediate hash. If a tile hash falls below a difficulty target, it is a valid proof of work.

- Because the noise has low rank, the original product A.B can be recovered from (A+E)(B+F) efficiently.

- A Plonky2 zkSNARK circuit then compresses this proof into a succinct verifiable output without revealing A and B.

The zkSNARK serves two purposes: compressing a potentially megabyte-scale proof into something lightweight, and preserving the confidentiality of the input matrices (which matters for commercial AI inference, where model weights and activations are proprietary).

This is a real cryptographic construction. It is anchored in a serious academic paper, IACR ePrint 2025/685, co-authored by Omri Weinstein (Princeton PhD, Hebrew University, NSF CAREER Award recipient) and presented at the Stanford Security Seminar in May 2025. The paper establishes formal security proofs and demonstrates an overhead of only 1+o(1) over naive matrix multiplication. That is not a whitepaper promise. That is a peer-reviewed mathematical result.

The codebase is a Go/Rust/Python monorepo, forked from btcd (Bitcoin’s Go implementation), with the SHA-256 PoW replaced by the NoisyGEMM kernel, a Plonky2 ZK prover in Rust, and a vLLM-based miner interface in Python/CUDA. For a project with 7 weeks of mainnet history, the technical depth is real.

2. The Together AI partnership: the first real signal

In May 2026, Pearl Research Labs announced a partnership with Together AI, one of the leading cloud inference providers in the current AI infrastructure landscape. The deal introduced a new endpoint for Gemma-4-31B-it at a 25% discount, funded by PRL emissions directed to the inference provider.

This is the first concrete implementation of the 2-for-1 model. An AI company runs real inference workloads, PEARL miners (in theory) execute those same matrix multiplications as mining work, and the mining rewards partially offset the inference cost. If this loop holds at scale, it is a structurally interesting economic model. The AI provider gets subsidized compute. The miner gets tokens for work that was already economically valuable.

I want to be precise about what this confirms and what it does not. It confirms that the technical integration is feasible. Together AI would not launch a production endpoint on a fake technical stack. The partnership validates the general architecture. What it does not confirm is whether the miners processing blocks on AlphaPool or LuckyPool are actually routing their GPU cycles through the vLLM miner interface and executing real inference. That is a different question entirely, and we will come to it.

3. The critical signal: ‘zero useful AI computation measured’

Let me be direct about the most serious finding in this analysis.

On June 3, 2026, a paper was published on arXiv (arXiv:2606.04819, Basu, NIELIT/IIITA) titled ‘The Usefulness Gap in Proof-of-Useful-Work: An Empirical Study of Pearl’s cuPOW Protocol’. The researchers spent approximately $50 in cloud GPU time to analyze 8,012 active workers on AlphaPool, PEARL’s dominant mining pool. A methodological note before going further: this is a preprint, not a peer-reviewed publication. The sample covers one pool only, and the methodology has not been independently replicated at the time of writing. I am not citing it as the final word. I am citing it because it is the only empirical measurement of on-chain behavior currently available, because the approach is transparent and reproducible, and because the team has not contested it. Those three facts together make it the most credible data point we have, pending a response.

Their finding: 100% of the miners analyzed were generating matrices via random number generation, specifically random_range(-64..=64), with no AI inference whatsoever. The dominant mining software (alpha-miner v1.6) contains no vLLM code, no inference pipeline, no connection to any AI workload.

This matters enormously for the investment thesis, so I want to explain exactly what it means and what it does not mean.

What it means: the PEARL protocol, as currently operated, is functionally equivalent to a standard GPU PoW using SHA-256 replacement. The ‘useful work’ is not happening. The hashrate (~24 EH/s at time of the study, representing an estimated 320,000 GPU-equivalents consuming ~112 MW) is producing zero AI value. The protocol verifies the correctness of the matrix computation, not its origin or usefulness. A miner using random matrices passes the same verification as a miner running actual Gemma inference.

What it does not mean: it does not prove the team is fraudulent. The paper cuPOW itself acknowledges that enforcing the ‘usefulness’ of the work is an economic problem, not a cryptographic one. The protocol was designed to allow useful work, not to mandate it. This is a fundamental tension in the PoUW design space that Weinstein’s paper explicitly discusses.

What it means for the thesis: the 2-for-1 value proposition does not currently exist on the live network. The narrative ‘Bitcoin of the AI era’ is aspirational, not descriptive of current on-chain reality. And critically, the team has not, as of early June 2026, issued any public response to the Basu paper.

I have been following this space since 2016, and I have learned to be suspicious of two things: projects that promise things that are physically impossible, and projects that stay silent when their core value proposition is challenged empirically. The second category is more dangerous because the silence is a choice.

4. Tokenomics and market structure: what the numbers say

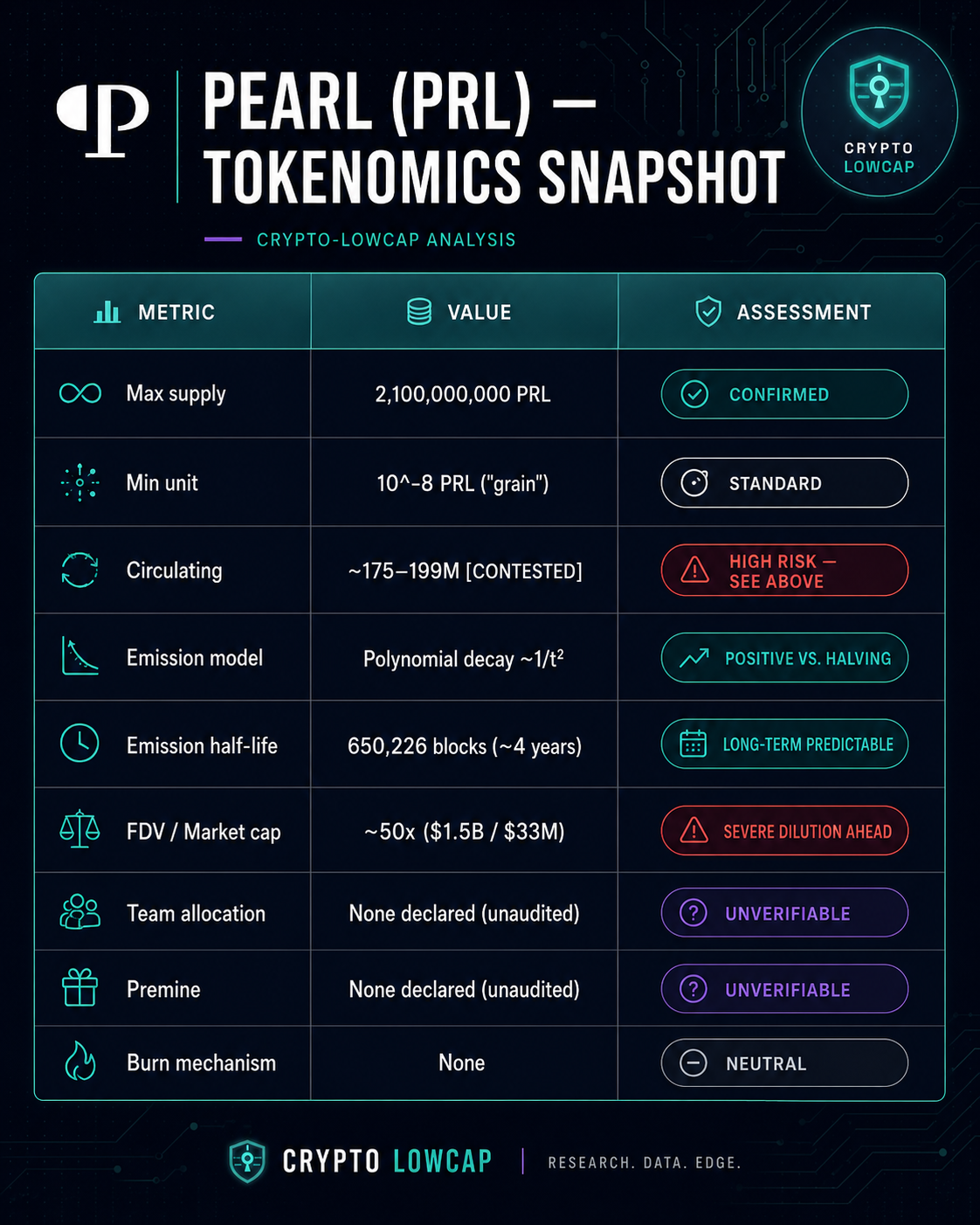

The emission model is one of PEARL’s more interesting design choices. Rather than Bitcoin’s halving schedule, PEARL uses a polynomial decay formula that produces a smooth, continuous reduction in block rewards. The half-life is set at 650,226 blocks, approximately 4 years, meaning about 50% of the total 2.1 billion PRL supply will have been emitted by ~2030. There are no shock events, no halving cliffs.

This is a thoughtful tokenomics design. The absence of halvings reduces the speculative mining rush and exit dynamics that characterize Bitcoin cycles. It creates a more predictable inflation schedule. That is a genuine structural advantage.

However, the macro numbers create a significant concern. The FDV/market cap ratio is approximately 50x. With ~175M PRL in circulation at a price around $0.65, the market cap sits around $33M. But the fully diluted valuation at 2.1B PRL is around $1.5B. That ratio implies extreme future dilution. Every holder today is holding against a horizon of 49x more tokens entering circulation over the coming decades.

The circulating supply figure itself carries an additional red flag. Both Upbit and Bithumb, two of South Korea’s premier crypto exchanges with rigorous listing standards, announced delays on their PRL listings explicitly citing ‘circulating supply concerns’. As of early June 2026, neither exchange has relisted. The project has not publicly clarified this discrepancy. That is not an acceptable state of affairs for a project claiming a fair launch.

Tokenomics summary

The FDV ratio alone is not a death sentence. Bitcoin’s FDV/market cap ratio at early stages was effectively infinite. What matters is whether the utility demand for the token grows faster than the supply expansion. For PEARL, that means the AI compute marketplace needs to generate real economic demand for PRL. Today, that demand does not exist beyond one Together AI integration. The ratio becomes dangerous if the project stagnates.

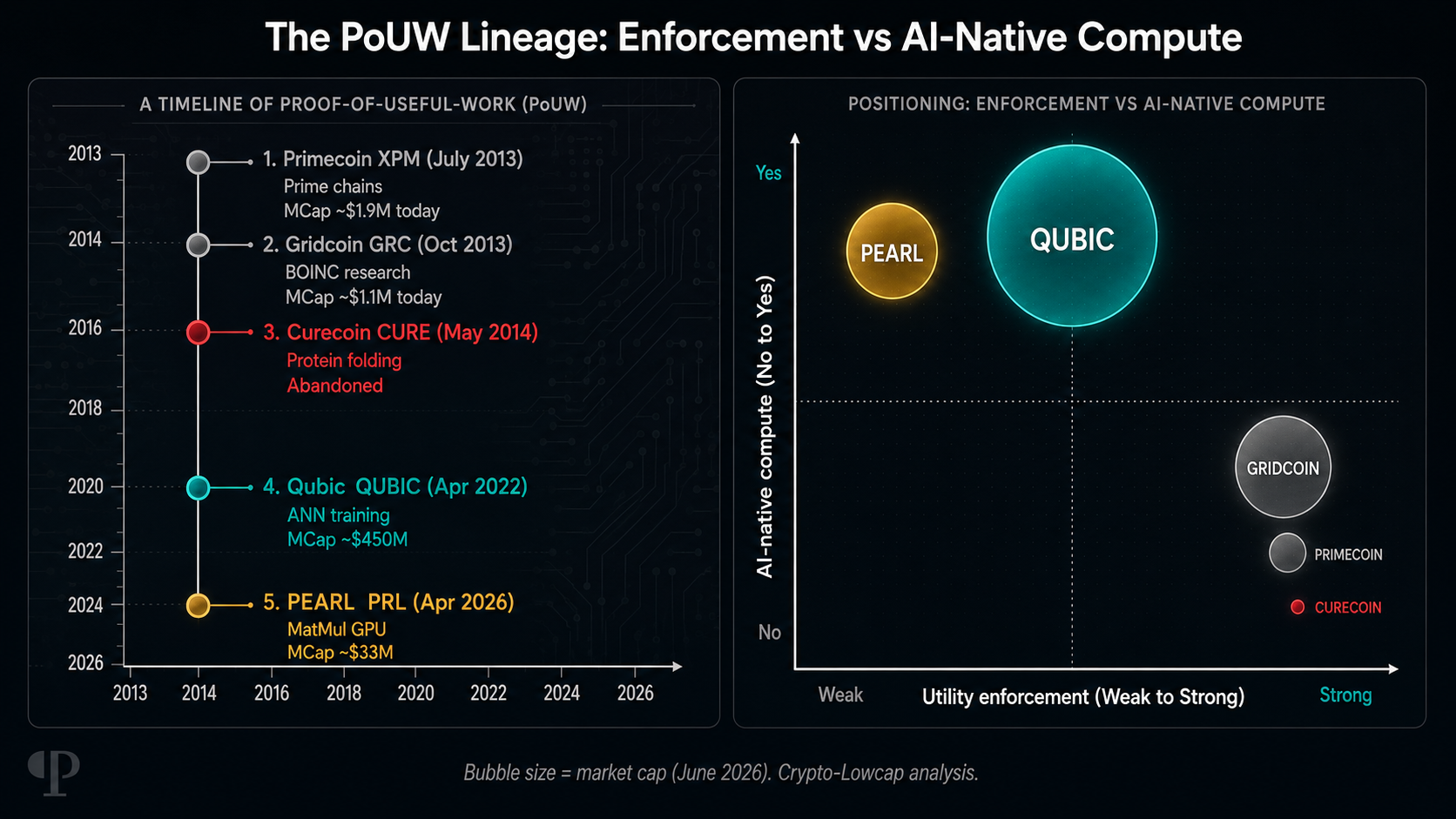

5. How PEARL compares to its real peers: the PoUW lineage

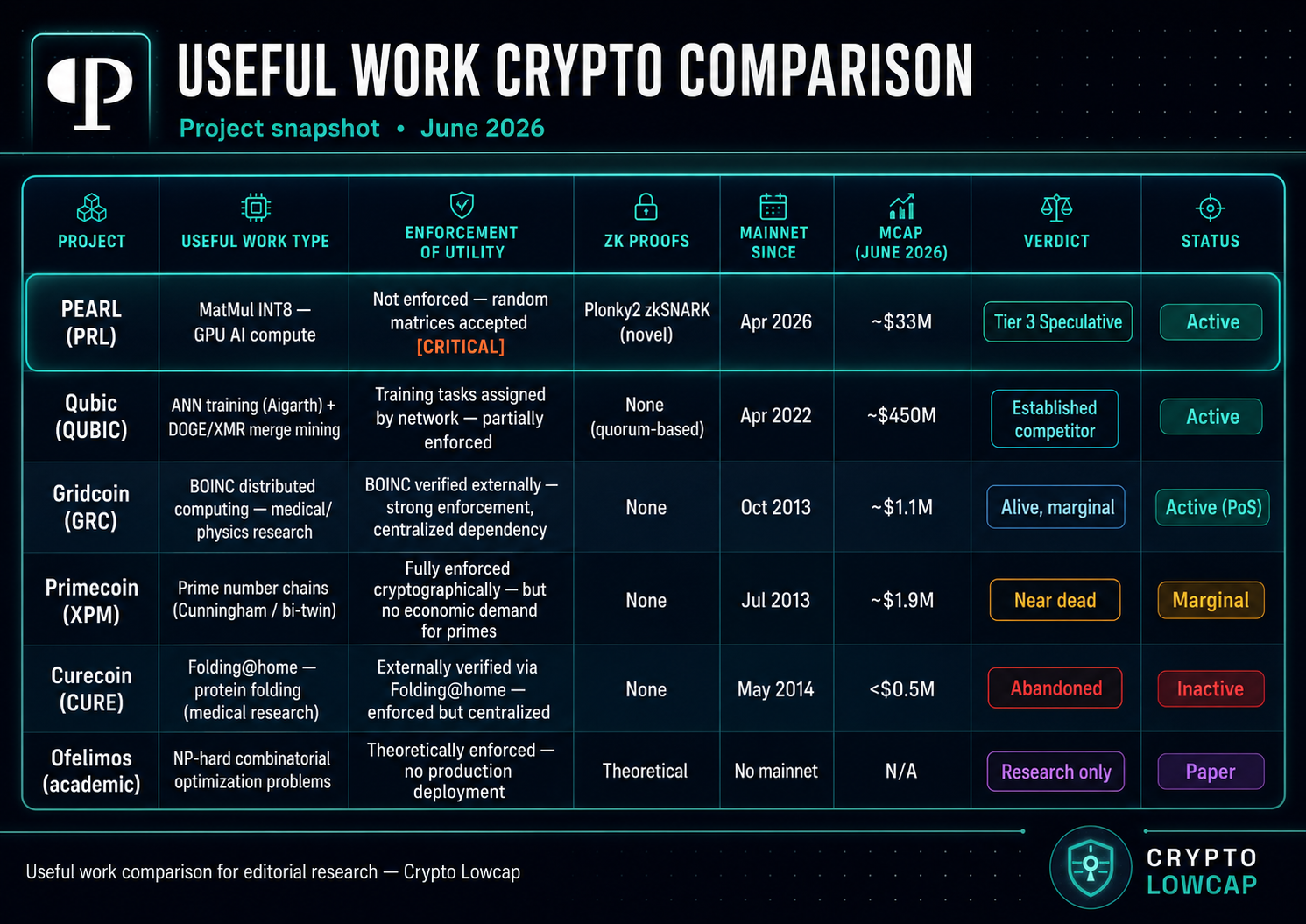

Let me be precise about one methodological point before the comparison. The relevant benchmark for PEARL is not Monero, Kaspa, or Aleo. Those are PoW or ZK-privacy projects with no relationship to the ‘useful work’ thesis. Comparing PEARL to them would tell you nothing analytically useful. The correct frame is the history and current state of Proof-of-Useful-Work specifically: the projects that have actually tried to make mining computationally productive, what they achieved, and why most of them failed.

That history is more instructive than any feature comparison with standard PoW chains, because the failure modes of PoUW are specific and recurring, and PEARL inherits them all.

Three structural lessons emerge from this table that map directly onto PEARL’s current situation.

First, the enforcement problem is the graveyard of PoUW. Primecoin solved it elegantly: Cunningham chains are inherently verifiable, no one can fake finding a prime. But the work generated zero external economic demand. Scientists did not pay for prime number chains. The token had no utility loop. Gridcoin took the opposite approach: outsource verification to BOINC, which carries real research demand. But that created a critical dependency on an external centralized infrastructure. If BOINC had shut down, so would Gridcoin. PEARL is trying a third path: cryptographically prove the matrix computation happened, while hoping the economic incentive will push miners toward genuine AI inference. The Basu study shows that hope is not yet reality.

Second, Qubic is the direct contemporary competitor, and it is substantially more advanced. Qubic has been operating since 2022, has a market cap roughly 14 times larger than PEARL’s, has an established community of over 630,000 members, has received a CertiK audit certifying 15.5M TPS, and has already demonstrated merge-mining of external assets (Monero, then Dogecoin from April 2026). Its useful work model assigns specific AI training tasks to miners through the Aigarth system, which is structurally closer to enforced utility than PEARL’s current approach. Qubic is not without its own risks — its consensus model (676 Computors, quorum-based) is far more centralized than Bitcoin-style PoW, and its ‘AI training’ claims around Aigarth remain contested — but as a benchmark for what a mature PoUW project looks like, it is the right comparison point. PEARL needs to answer the question of why its approach is meaningfully better than Qubic’s.

Third, the historical base rate for PoUW projects is poor. Primecoin: near-dead at $1.9M market cap despite 13 years of existence. Curecoin: abandoned. Gridcoin: surviving but marginal at $1.1M. Qubic: the outlier success story, with a genuine community and real technical progress. The PoUW category has produced one meaningful survivor out of five known attempts. PEARL enters this field with a better academic foundation than any of its predecessors, but also with the most unresolved fundamental question: is the useful work actually happening?

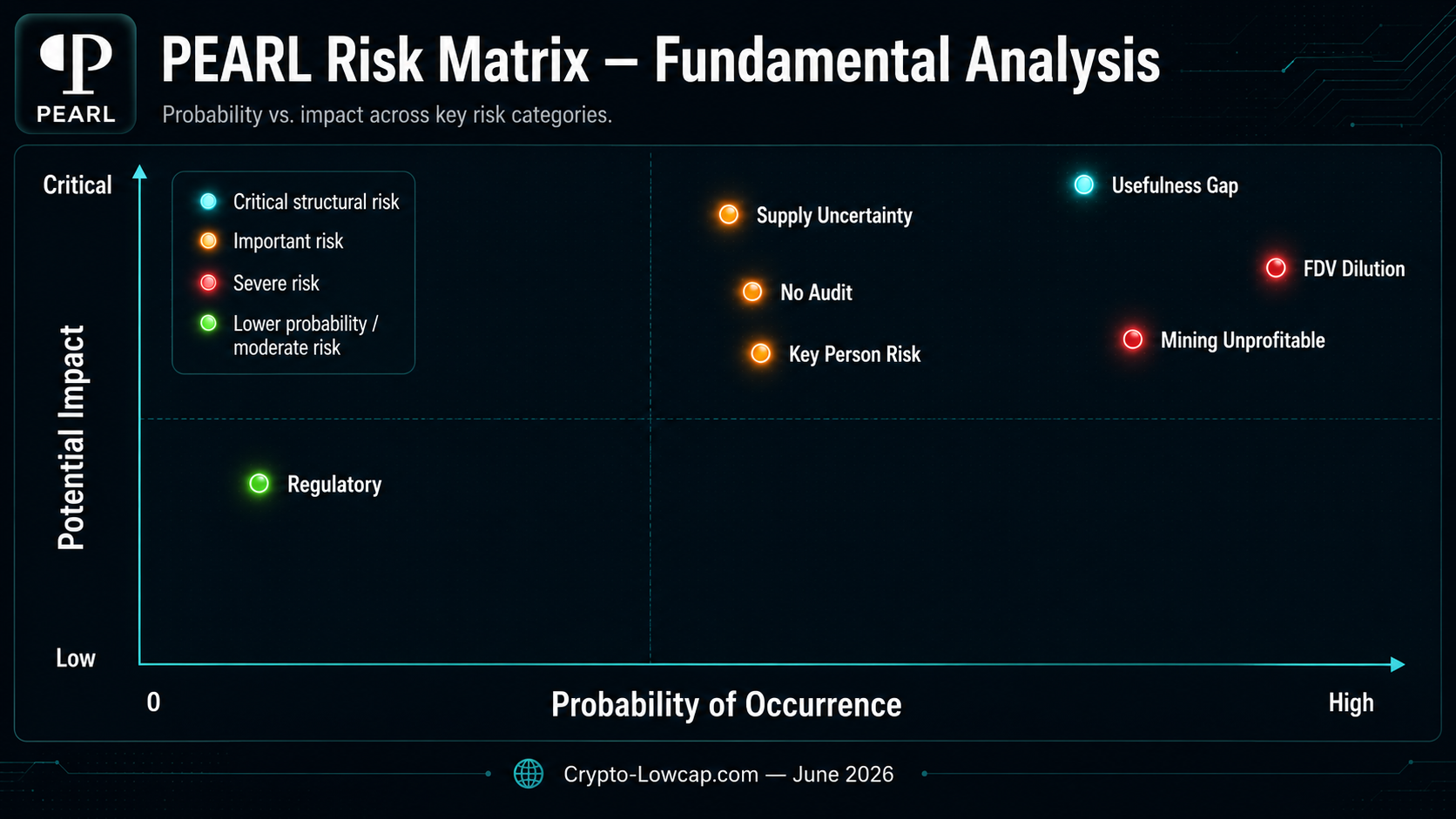

6. Risks: what could go wrong

I will not pretend these are minor concerns. For a project this young and this speculative, the risk list is long and several items on it are serious.

The usefulness gap — Critical

This is the central risk and it is qualitative, not just technical. The protocol does not enforce useful computation. Miners use random matrices and pass verification. Unless the team implements a mechanism to incentivize or verify actual AI workloads, PEARL is a GPU PoW with an elaborate story. The fact that they have not publicly responded to the Basu study as of early June 2026 makes this risk more, not less, concerning.

Circulating supply uncertainty — High

Upbit and Bithumb did not delay their listings over a clerical error. These are Tier 1 South Korean exchanges with rigorous compliance frameworks. Their explicit reference to ‘circulating supply concerns’ is a material flag. If the actual supply differs from what is declared, or if there is an undisclosed team/VC allocation that was never announced, the fair-launch narrative collapses. This must be resolved with on-chain transparency before any confidence in the tokenomics is warranted.

No external audit — High

There is no published security audit of the NoisyGEMM protocol, the Plonky2 circuit implementation, or the overall codebase. ZK circuits are among the most complex and audit-sensitive components in blockchain engineering. Plonky2 itself is a cutting-edge proof system. Deploying it in production without an audit from a firm like Trail of Bits, Zellic, or NCC Group is a meaningful structural risk.

FDV/Market cap ratio ~50x — High

At current prices, the fully diluted valuation is roughly 50 times the circulating market cap. Over the coming decades, the polynomial emission schedule will mint 1.925 billion additional PRL. Every holder today carries the full weight of that dilution. Without a massive expansion of economic demand for PRL, the price pressure from emission will be structural and persistent.

Mining profitability negative — High

The empirical Basu study calculates a negative ROI of -54% to -72% for GPU miners at current prices. Miners with cloud GPU rentals are operating at a loss. This creates persistent sell pressure as miners dump rewards to cover costs, and risks a significant hashrate exit if the price stays at current levels. A hashrate collapse would reduce the security of the network and could make it vulnerable to 51% attack scenarios.

Key-person concentration — Medium-High

Omri Weinstein is the only publicly identified founder. The remaining 7+ contributors on GitHub are either anonymous or not publicly associated with the project. The project’s credibility rests heavily on his academic reputation. Any reduction in his involvement would have a disproportionate effect on market confidence and development continuity.

Regulatory risk — Low to Medium

Pure PoW projects have generally fared better under regulatory scrutiny than ICO-based tokens. That said, the team structure (‘Pearl Research Labs’) is not formally documented, and the project’s jurisdictional footprint is unclear. MiCA compliance for a non-EVM PoW coin is less urgent than for smart-contract platforms, but the energy consumption angle remains a political liability in the EU context.

7. What would change my conviction

I want to be clear: I am not dismissing PEARL. The academic foundation is genuinely unusual for a project at this stage. What I am saying is that the thesis is not yet validated in practice, and several risks are unresolved. Here is what I would need to see to upgrade my view.

Short-term signals (0-3 months)

- A public response from the team to the Basu study. Not a dismissal, a technical engagement. Either demonstrate that useful work is occurring, explain why the Basu methodology was flawed, or commit to protocol changes that will enforce it. Silence is not an acceptable answer when your core proposition has been empirically challenged.

- A transparent on-chain accounting of the circulating supply, including an analysis of the genesis UTXO set. Upbit and Bithumb listing resumptions would be a strong proxy signal for resolution.

- An announced external security audit by a recognized cryptographic auditing firm.

Medium-term signals (3-12 months)

- The FP8/BF16 floating-point extension. Currently, NoisyGEMM operates on INT8 matrices. Most modern AI inference runs in FP8 or BF16. Without this extension, the protocol cannot natively integrate with the bulk of current AI workloads. The whitepaper acknowledges this as a future upgrade; actual delivery would be a significant positive catalyst.

- Additional AI compute partnerships beyond Together AI. One integration is a signal. Three integrations are a trend.

- Publication of the IACR paper in a peer-reviewed conference proceedings (CRYPTO, EUROCRYPT, CCS). The paper was presented at Stanford, but publication in a major venue would substantially increase academic credibility.

Long-term (12+ months)

- A functioning on-chain compute marketplace where AI inference workloads are matched with miners in a verifiable, economically rational loop. This is the ultimate test of the thesis. If Pearl achieves this, it has created something genuinely new in the crypto space.

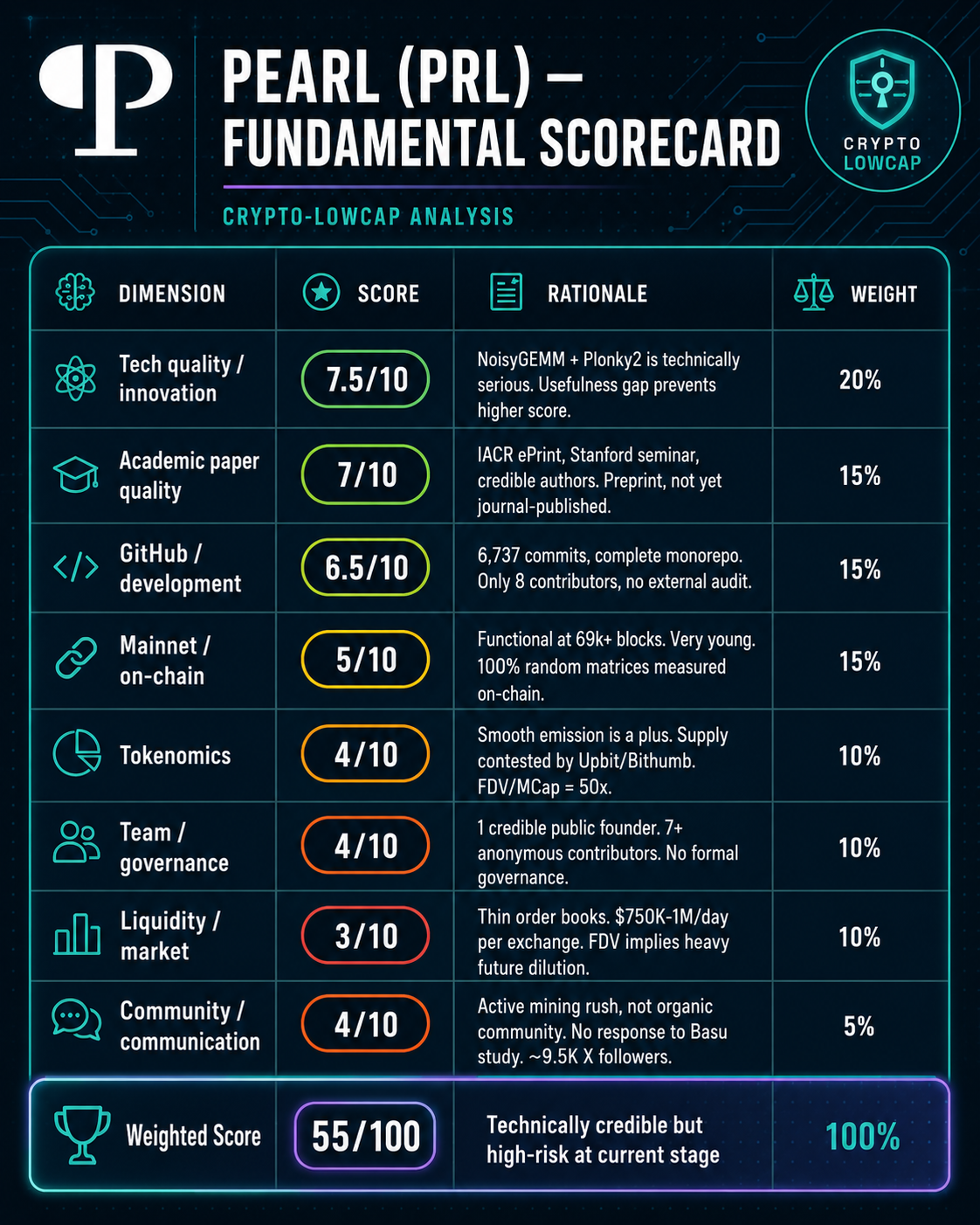

8. Fundamental scorecard

Verdict: speculative frontier, real technology

I will not hide my interest in the project as a technical construct. PEARL is doing something no one has successfully deployed in production before. The cryptographic machinery is legitimate. The academic foundation is real. The team knows what they are building.

But I have also watched enough promising PoW projects fail to recognize the pattern. Primecoin had elegant mathematics and failed to create economic demand for its prime-number outputs after 13 years. Curecoin and Gridcoin outsourced the utility verification to external platforms and became hostages to those platforms’ survival. Qubic, the closest operational analogue, has grown to a $450M market cap but remains contested on whether its AI training outputs constitute genuine scientific value. PEARL’s risk is structurally familiar: a technically valid proof of useful work that is not, in practice, being used for anything useful on the live network today.

The thesis could still materialize. If the FP8 extension ships, if the compute marketplace launches, if additional AI providers follow Together AI’s model, PEARL could evolve into something genuinely significant. The ‘Bitcoin of the AI era’ narrative is one of the most powerful available in the current macro context. If the substance catches up with the story, this becomes a very different analysis.

But today, in early June 2026, with the Basu study unaddressed, with supply figures disputed by Tier 1 exchanges, with no external audit, and with mining currently unprofitable, PEARL is a Tier 3 speculative position. The potential is real. The execution risk is enormous. The appropriate position size is minimal, and only for those with the risk tolerance for early-stage, unaudited, single-use-case L1 projects.

Watch for the Basu response. Watch the supply resolution. Watch the FP8 announcement. Those three signals, more than any price action, will tell you whether the thesis is alive or dead.

| CONVICTION TIER : TIER 3 — Speculative Rationale: Real academic foundation and first production PoUW implementation, but core ‘useful work’ thesis is currently unsubstantiated on-chain. Supply opacity and absence of external audit create unacceptable uncertainty for a fundamental position. Bull case: FP8/BF16 extension ships, compute marketplace beta launches, Basu study receives a credible technical response, supply is transparently audited, and additional AI partnerships are announced. Bear case: Usefulness gap persists, team stays silent on Basu findings, supply remains unresolved, Upbit/Bithumb listings remain delayed, no audit in 6 months. Conditions for upgrade: Delivery of FP8 extension + external security audit + supply transparency + 2nd major AI partner. All four, not one or two. |

Key takeaways

- The FDV/market cap ratio of ~50x implies massive future dilution. Mining is currently unprofitable, creating structural sell pressure.

- Conviction Tier 3 (Speculative). Minimum position. Maximum curiosity. Monitor the three signals outlined above.

Useful Links

crypto-lowcap.com | Revealing Privacy. Defending Sovereignty.

Follow @CryptoRowenta01 on X | Subscribe to the newsletter